Dambisa Moyo has written a book that fails to deliver on a great title: “How boards work and how they can work better in a chaotic world”[1]. Her own website describes her as “a pre-eminent thinker, who influences key decision-makers in strategic investment and public policy…respected for her unique perspectives, her balance of contrarian thinking with measured judgment, and her ability to turn economic insight into investible ideas”. Her book is not the place to test the final claim. However, the bold title of this book suggests that it might provide some evidence for the other claims but there is precious little.

Despite having served on the boards of SABMiller, Barclays Bank, Barrick Gold, Seagate Technology, 3M, Chevron, and a couple of charity boards, her account of board operation is pedestrian and, possibly because she is reluctant to bite the hand that feeds her, is merely descriptive but without providing either light and shade or texture. It is frustrating that with a CV that suggests that she might actually be quite smart, her account of corporate governance is pitched at the level of a US college freshman, without any discussion of alternative models of board structure and board purpose (not even of the Anglo Saxon model on the other side of the Atlantic with its unitary model including substantial executive presence and the statutory obligation to consider all stakeholders under Section 176 of the UK Companies Act).

For someone who bills herself as a contrarian with unique perspectives, the changes in society that she suggests are evidence of a “cultural revolution” entering the boardroom have been mainstream for a generation (once again, little recognition of the progress made in increasing the representation of women in the board room or the degree to which changes in wider society have entered into boardroom debate – notwithstanding the survival of some dinosaurs and dinosaur attitudes). Her account might have been a cultural revolution had she been writing in the time when Young Pioneers were waving copies of the Little Red Book, but she does not appear to be on the bleeding edge of change in the third decade of the 21st century. Likewise, as increasing numbers of corporate leaders are signing up to environmental responsibility and addressing climate change and the Business Roundtable’s Statement on the Purpose of a Corporation has been around for eighteen months, her prescriptions, though sound, are hardly earthbreaking.

One of the corporate leaders who has provided an endorsement on the dustcover describes this as “not only a must-read for the most tenured and experienced board member, but it also provides critical context for those who one day hope to have a seat at the table. CEOs and corporate leaders everywhere would also be wise to pick up this book.” I can only assume that this individual didn’t read the book herself – probably quite a sound move had she not chosen to perjure herself by writing such a ringing recommendation.

[1] Moyo D. (2021) How Boards Work London: The Bridge Street Press

On 26th June 2020 99% of the shareholders in Danone voted for it to become an enterprise à mission, or purpose driven company, required not only to generate profit for its shareholders, but do so in a way that it says will benefit its customers’ health and the planet.

Less than nine months later, Emmanuel Faber, Danone’s chief executive and the architect of the new strategy, was ejected by the board in the face of pressure from activist investors. The FT leader writer observed on 18th March that “a backlash against purpose-driven capitalism was overdue” and that the debacle was “a reminder that distractions from the core goal of making a profit can be dangerous” before concluding that it did “not …. signal that leaders should rein in their ambition to go further and reassert the role of companies in society” and that to “revert now to simplistic and damaging pursuit of crude share-price maximisation would be a mistake.”

The ejection of Faber was not an illustration of the primacy of Friedmanite shareholder value, but an example of a chief executive failure to manage the investor market interface. We don’t know precisely what the activist investors were thinking, but they were clearly dissatisfied with the returns they were expecting and believed that their investment returns would be increased with a different chief executive.

Under Faber’s successor, the activist investors hope that the value of their investment (in terms of capital growth and dividend returns) will increase as a result of improved internal operational performance and a changed strategy towards the customers at its other market interfaces – including suppliers, employees, consumers, owners of real estate and local communities, regulators, and government (recalling the appetite of the French government to view large domestic consumer businesses as strategic national assets when threatened by acquisition by overseas multinationals). The choices of the different types of customer will include some consideration of ESG: consumers with an eye to environmental consideration (packaging, use of sustainable resources; employees preferring to work for companies whose conduct they can take pride in; investors wanting to see good governance. The rhetoric employed by the activist investment customers may reflect discontent with financial returns, but implicitly they are concerned with how the Danone’s mission is translated into strategy and the possibility that Faber’s rhetoric around purpose conceals a lack of grip on operational performance.

The Danone debacle generated further commentary on whether this apparent backlash represented a retreat from “purposeful capitalism”. John Plender wrote a powerful article for the FT on 4th April reflecting both on the Danone story and on the lessons from the Covid about the impact on stakeholders (particularly suppliers) who were unable to diversify their risk (unlike investors) when a business hit rocks as the pandemic closed down parts of the economy. He shared the view, which we addressed during the debate in 2017 on corporate governance reform in the UK, that appointing employee directors (or by implication directors representing any other specific stakeholder group) does not address the governance gaps. He went on to argue for changes to the incentive models for senior managers to address short-termism and that profit or share value metrics determining them should be supplemented by ESG related metrics. In short, “stakeholder capitalism must find ways to hold management to account” and that “the prevailing commitment to short-termist shareholder value has undermined corporate resilience.”

Hakan Jankensgard, Associate Professor of Corporate Finance at Lund University responded to Plender in a letter published by the FT on 7th April with an assertion that the firms should adopt the Hippocratic oath since this “would ensure that firms act as good corporate citizens”, with focus on long term profitability and “not become do-gooders picking sides in social debates”. It is probably a reflection of the challenge of drafting a letter of appropriate length for publication, but some steps in his logic seems to missing. However, other parts of his letter are compelling, echo arguments within the Escondido Framework view on how firms work and pitfalls in contemporary corporate governance, and are worth producing in full:

“As far as everyone is concerned, shareholders are the root cause of all the troubles afflicting our societies.

“Well, think again. The real problem today is managerial capitalism – that managers run firms primarily to increase their own wealth and prestige. A few decades back, managers were busy building wasteful empires, and the shareholder model arrived as a particular remedy for this gross inefficiency.

“Another innovation that arrive about the same time prove more fateful. It was the idea that managers, if given the right financial incentives, would rediscover their entrepreneurial spirt. It caught on, to say the least. What it really did, however, was to shift managers’ focus from building empires to extracting wealth through compensation packages.

“As manager took n their new role, they found willing accomplices in a cabal of short-term oriented investors looking for a quick return. This unfortunate marriage is the problem at the heart of today’s economy as it creates short-termism that adds to long-term risk.”

Chartists meet on Kennington Common in 1848 – the year of the Communist Manifesto and “All things bright and beautiful”

I went into the first Covid-19 lockdown in March with three doorstep sized volumes to keep me going.

The 912 pages of Hilary Mantel’s Mirror and the Light were riveting, even if I knew from the outset that Thomas Cromwell’s career would come to an abrupt end at Tower Hill in 1540. The 1088 pages of David Abulafia’s magisterial The Boundless Sea kept me entertained as it opened my eyes, chapter by chapter, to the way that different parts of the world became progressively connected by maritime exploration, communication and trade.

I had started turning the 1041 pages of Thomas Piketty’s Capital and Ideology before restrictions started to be lifted in May but, despite finding some stimulating ideas in his opening account of the different sources of power of different parts of premodern society (which he describes as ternary or trifunctional, and have echoes in the Escondido Framework’s account of the three currencies or sanctions), it was not until the re-imposition of lockdown (the UK government’s Tier 4 restrictions) that I finally completed it.

I admire much of what Piketty has done in Capital and Ideology. His effort to document the movements in the shares of income and wealth between different groups in different societies throughout human history, and particularly the past century or so, is admirable and revealing. It is possible to challenge some of his assumptions and definitions, but the picture he paints of the direction of the trends in material inequality are compelling. I agree with his spin on Rawls’s maximin principle: “To the extent that income and wealth inequalities are the result of different aspirations and distinct life choices or permit improvement in the standards of living and expansion of the opportunities available to the disadvantaged, they may be considered just.” (p.968). His chapters on the increasing support of the “Brahmin” classes educated to degree level for parties of the left and the corresponding “Nativist” alignment of parties of the traditional right and “left-behind” communities are persuasive. But the book is far longer than it needs to be, many of its graphs add little, and he strays from the professorial scholarship of the economist/social scientist-turned-historian into an undergraduate level of prescription.

Piketty’s underlying thesis is that “no human society can live without an ideology can live without an ideology to make sense of its inequalities.” I didn’t need to read 1041 pages to recognise this: growing up in a churchgoing family, I remember singing the third verse of “All Things Bright and Beautiful”

The rich man in his castle,

The poor man at his gate,

God made them, high and lowly,

And ordered their estate.

These days, it is generally omitted!

It may or not be a coincidence that Mrs Cecil F Alexander wrote these words in 1848, the “Year of Revolutions”, in which Marx and Engels also wrote The Communist Manifesto. Piketty chooses to reformulate the opening words of its first chapter “The history of all hitherto existing society is the history of class struggles” as “The history of all hitherto existing society is the history of the struggle of ideologies and the quest for justice.”

There is something in Piketty’s thesis about the relationship between the ideas that prevail at any point in time and the organisation of society and its impact on the distribution of wealth and income. It may be that I started out as a historian whereas has come to history by way of economics, but I find that he oversimplifies to sustain his argument. Ideas ebb and flow and they can influence behaviours, but this is not the same thing as saying that they determine behaviours. He falls into the trap of assuming that the behaviours that are generally ascribed to “capitalism” are the product of the past few centuries.

He frequently quotes Karl Polanyi with approval, who was even more blinkered in this respect, regarding capitalism as an entirely modern phenomenon. Peter Acton has undermined Moses Finlay’s thesis that the ancient economy was shaped by considerations of status and civic ideology rather than rational economic considerations, demonstrating in Poiesis: Manufacturing in Classical Athens demonstrates that the commercial decisions of Athenians “were for the most part…consistent with today’s understanding of good (rational, profit-maximising) business practice[1]. It does not require a 21st century reading of the biblical parable of the talents to see that the notion of investing for a return was established by the time the Christian gospels were written. And Abulafia’s The Boundless Sea, contains plenty of evidence for the commercial underpinning of the development of maritime trade over many centuries. One of the primary shortcomings in Polanyi’s approach was that set very specific conditions around anything that he would define as a market and, by framing his argument in this way, created a platform for his dismissal of the longstanding heritage of commercial activity. It is as though Polanyi, and to a lesser extent Piketty, seek to dismiss market mechanisms and their place in human societies on the basis that, prior to Adam Smith and his successor, the conditions assumed in classical economics had neither been articulated nor did they prevail.

Essentially, it is not that Piketty is wrong, but his case is overstated and needs reframing. It is not that ideology determines the form of economic organisation, but it helps shape relationship between the parties. In Escondido Framework terms, the prevailing ideological frameworks will influence the attitudes and trade-offs made by parties in their relationships with each other at market interfaces. For example, a religious ordained prohibition on usury does not undermine the human behavioural drivers for gratification today over gratification tomorrow and discounting for risk (although these can be culturally influenced), but historically has resulted in work-arounds (eg Islamic finance) or lending being undertaken by a community less constrained by the prohibition. Certain activities, as in caste based societies, may be undertaken by tightly defined social groups, with implications for the commercial terms on which these activities take place. But this is not the preserve of caste societies: while the boundaries may be less clearly defined and not religiously ordained, even in contemporary society there is an intergenerational stickiness in occupations and values, traditions and attitudes acquired in childhood shape occupational choices and behaviours.

So, two cheers for Picketty for the underlying thesis. And, in due recognition of his own disclaimer in his concluding chapters, he has set out to provoke further debate and provide the foundation for further scholarship rather than provide the definitive answer

However, where I find Capital and Ideology most flawed in when Piketty moves from diagnosis to prescription. In particular, his leap from describing to the increasing inequality in economic outcome for the richest few percent compared to the poorer mass of the population to concluding that all would be solved by appointing worker representatives to corporate boards highlights the danger of straying too far from your own area of expertise.

The inequality that Piketty documents arises from the endowments that we start out with in life (geography, genetics, family wealth, upbringing, education) and our life choices and chances (too many possibilities to enumerate). These will shape whether we end up with investable wealth (the impact of this on equality is thoroughly documented in his earlier work: Capital in the 21st Century) and whether we end up in positions in which we have market power and are able to extract economic rent, which has arisen most egregiously in recent years for executive directors of large companies as a result of shortcomings in corporate governance. Addressing inequality arising from our endowments needs primarily to be by “levelling up” in terms of investment in education and social support, particularly in early years, and widening opportunities, but in relation to inherited wealth is a proper area for taxation. Addressing inequality arising from investable wealth is also clearly an issue for taxation and also needs international solutions, but is a complex matter not least because of the risk of creating perverse incentives and unintended outcomes. Taxation has its place in addressing inequalities in income, but as with addressing issues surrounding taxation of wealth and wealth transfer, is also fraught with difficulty. Piketty raises these issues quite correctly.

But addressing inequality arising from market power and the ability to extract economic rent is a proper matter for better corporate governance and regulation to address market failure. Piketty fails to recognise the role of market failure and consequently the need to address this, and also the problem of the increasing ability of corporate management (and some of the services that support them), to extract economic rent (ironically, at least in part, at the expense of the owners of investible wealth), and that this is purpose behind the need for reform of corporate governance. His own prescription, worker representation on boards, is not the solution for reasons that I have argued elsewhere. Rather, and this comes back to his underlying thesis around ideology, there is a need to widen the understanding about the proper purpose of the company (the core of the Escondido Framework), and an improved understanding of the role of boards in serving them.

[1] Acton P (2014) Poiesis: Manufacturing in Classical Athens. New York: Oxford University Press

Dame Vivien Hunt, until this year managing partner of McKinsey’s offices in the UK and Ireland, has written in today’s Financial Times on workplace diversity and equality under the heading “Change how boards work to achieve to true diversity”.

She asks why, when one third of the seats on the boards of FTSE 100 companies are now occupied by women, “those boards still look similar……still filled with people who have the same skills carved out of similar professions, networks and university degrees.” Her explanation is that it is “because they still do the same thing: they primarily serve shareholders.”

I am pleased that one of the current leaders of the organisation where I started my professional career takes such an unambiguous and very public position strong position on both the composition of boards and their purpose. Back in the 1980s, most of my colleagues were beholden to the orthodoxy of “shareholder value” and, although there were a small number of senior non-white consultants (including Keniche Ohmae, who led the Tokyo office, and Rajat Gupta, who became an office managing partner shortly after I left and subsequently global managing partner), the firm was anything but diverse.

Dame Vivien argues that “we need to find people who represent not only our investors but everyone else – from buyers to suppliers, to local communities, to our natural environment”. Her use of language and her argument is not entirely clear here: her article could easily be interpreted as making a case for a board of representatives of stakeholders as opposed to a board that understands the broader mandate of the company and the need to take all stakeholders’ interests into account.

I have argued elsewhere against boards being composed of representatives of stakeholders. As is implicit in Dame Vivien’s article, directors should have a duty to all stakeholders, because their wellbeing of all groups is critical to the wellbeing of the company. Furthermore, in UK unitary boards composed of executives and non-executives, at the board may be the executive directors responsible for sales and marketing who should be the effective advocates for interests of consumers if they are fulfilling their role understanding and satisfying consumer needs. Similarly, executive directors of workforce and of operations should be able to represent to colleagues, who may place a primacy on the interests of shareholders and customers, the interests of the people they recruit, support, and manage. Whether or not they are full board members, most large companies employ directors of communications and public affairs (or similar) whose primary role may be to advocate externally for the company but also represent to the board the case for taking into account the interests of local communities, the environment, politicians and lobbyists.

I was thrilled to read Dame Vivien’s piece and pleased to see her continued work championing diversity in business. But, notwithstanding my concern about some of the logical flow and detail in her argument, I was even more encouraged to see her set out the case that genuine diversity on boards will not be achieved until shareholder primacy is consigned to the waste bin.

With their decision to resign as auditors to Boohoo after seven years, PwC’s partners have at last shown that they are willing to say boo to a goose. Ditto those at Deloitte, who quit as auditors to EG, the petrol station operator that has agreed to relieve Walmart of Asda (albeit with a big slug of vendor finance). And their colleagues at Grant Thornton who, prompted by a probe by the Belgian tax authority, decided that they had had enough of dealing with Mike Ashley at Fraser Group (better known as Sports Direct). And those at EY, who quit from auditing Finablr in May over weaknesses in corporate governance and links to troubled NMC Health.

This is welcome news, given that the Financial Reporting Council observed in November last year in its annual “Developments in Audit” publication:

“Audits are not consistently reaching the necessary, high standards required to provide confidence in financial reporting.

“A series of high-profile corporate failures has dented trust in the profession and highlighted the need for improvement……

“Our 2018/19 AQR inspections show auditors still struggle to challenge management sufficiently.”

The final point is nothing new. I worked alongside one of the big firms in the early 1990s, undertaking a review of branch level financial controls (which were not as good as they should have been) in the largest chain in a quoted retail group. I recall attending a meeting alongside the audit partner with the chief executive, a “strong personality”, and observed him forcefully objecting to proposals for qualifying the accounts. I understand his reasons for doing so, and have in the past made a similar argument to an auditor to persuaded them that my organisation passed the “going concern” test. However, the shocking aspect of this case was observing the chief executive drawing the commercial value of the advisory business attention of his company to the audit firm to the attention of the audit partner, that the subsequent audit opinion was not qualified, and that the company collapsed within six months.

Kate Burgess, writing in the FT today, suggests that the decision by PwC is a calculated commercial decision rather than motivated by principle. She suggests that as the revelations about Boohoo’s employment practices emerged the reputational risk from being its auditor exceeded the value of the £389,000 annual fee income. This may be harsh, but few in the audit profession can forget what the relationship to Enron (although it may have amounted to more than guilt by association) did to Arthur Anderson, and noting that EY’s partners must remain anxious about potential impact on the company of its involvement with Wirecard.

Irrespective of the motivation, the decision of audit firms to step back from working with clients who do not have adequate controls and who may well operate unethically can only be welcomed. And even if progress can seem glacially slow, the action of regulators in trying raise standards must be welcomed too.

What better illustration could there be of the Escondido Framework approach to understanding ESG investing described in last week’s blog than the defenestration of Rio Tinto’s chief executive, Jean-Sebastien Jacques, by the company’s shareholders?[1]

In relation to the distinction made in last week’s article between the impact of regulation on the solution space available to executive teams, one of the interesting aspects of the dynamiting of Juukan Gorge and the two rock shelters is that the company had previously negotiated native title agreements with the Puutu Kunti Kurrama and Pinikura people, giving it rights to mine the area and had also secured regulatory approval. In Escondido Framework terms, as illustrated in last week’s blog post, the company thought that it was operating within the solution space defined by the market transaction with the owners of the land and that the regulatory market interface had not reduced the solution space available to the company.

However, the executives had failed to appreciate the sensitivities of the company’s investors to such an egregious violation of the heritage of not only the indigenous population but humankind as a whole.

Perhaps the board and executive team at Rio Tinto paid too much attention to the likelihood that investors in mining stocks are already a self-selected group that is less sensitive to ESG considerations than the investment market overall.

It matters little whether the response of the investors whose pressure on the board finally persuaded chairman Simon Thompson (who previously had insisted that Rio Tinto would not fire Mr Jacques) was a reflection of the potential for the scandal to increase future regulatory pressure on the industry, or a concern for the response of the upstream investors in their funds, or the consciences of fund management executives themselves being pricked by comparisons between the dynamiting of the caves with the actions of the Taliban blowing up the Bamyam Buddhas in 2001.

Either way, the shape of the investment market interface was sufficiently different to that perceived by Mr Jacques and his colleagues for them to have placed themselves, not temporarily but at a personal level permanently, outside the solution space available to them.

[1]For anyone who missed the story, Rio Tinto blew up two 46,000-year-old Aboriginal rock shelters in Western Australia, offending not only the Australia aboriginal community for whom the sites were sacred but also a wider public sensitive to an ancient archeological heritage. Initially the board decided to withhold bonuses for the executives involved, but has now decided that Mr Jacques should go (albeit not until early next year and without any further financial penalties)

The Financial Times has published a flurry of articles and the occasional letter about ESG (Environmental, Social and Governance) investing recently.

For example, Geeta Aiyer, president of Boston Common Asset Management, was the subject of a profile on 29th August. This followed the success of Boston Common and other investors to secure the change of name of the Washington Red Skins American Football team by applying pressure on FedEx, the logistics company which sponsors the team’s stadium.

On 1st September the paper published an article about write-downs at BP and Shell in response to “scores of asset managers who have doggedly pressed the oil companies to set targets to reduce carbon emissions and recognise the financial impact climate change could have on their operations” . The article cites a number of leading fund managers who comment on the “explosion” in ESG investing. It also notes the role of regulation in changing perspectives, citing the requirement now placed on pension fund managers in the UK take sustainability issues into account in their investment decisions and the impact of the EU’s sustainable finance package which will, from March 2021, push asset managers to incorporate ESG risks in their decision making.

A day later, on 2nd September, the FT published an article by Chuku Umuna, former Labour business spokesman and now lead for ESG with Edelman, the public relations consultancy, arguing that “a company’s ability to manage ESG factors is widely viewed as a proxy for prudent risk management, and with good reason”, citing work by Société Générale on the impact of ESG-related controversies that found that “in two-thirds of cases a company’s stock experienced sustained underperformance, trailing peers over the course of the following two years.”

A few months earlier, on 9th July, Gillian Tett wrote an article that opened by observing that the major ESG indices in the US and in Asia had outperformed the equivalent all share indices in terms of the financial returns to shareholders and cited a report from BlackRock making the same case, not only in the past year but also in 2015/16 and in 2018. BlackRock put this down to two primary reasons: the momentum created by ESG investors pushing up prices as they seek to acquire these stock for their clients and beneficiaries; and the value to companies seeking to improve their ESG ratings the scrutiny to which they subject their supply chains and employee practices and the consequent benefits that arise to their businesses.

Does the Escondido Framework approach to understanding organisations help us understand what is going on?

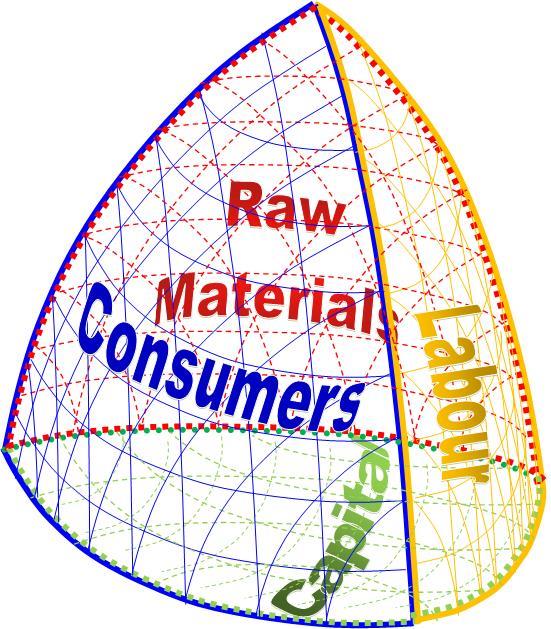

The Escondido Framework approach to looking at the firm is described in detail elsewhere. In essence, it explains that firms exist as a virtual space defined by their market interface with the suppliers of capital, labour, suppliers of goods and services, and customers, plus others whose needs may need to be satisfied, such as government or the wider community who implicitly or explicitly provide the firm with a license to do business. Their survival depends on creating value through the efficiency of their internal operations for there to be such a space. Where the firm places itself within the space will determine the distribution of economic rent to the stakeholders, how much may retained by the executive management, and how is available for reinvestment either in assets or long term relationships with one of more sets of stakeholders. As the market interfaces changes – through changes in supply and demand, competition, or the trade-offs made by the other parties to the markets place exchange – the virtual space (which can also be considered as the solution space available to the management team) may expand or contract (increasing or reducing the range of options, strategies and potential profitability available).

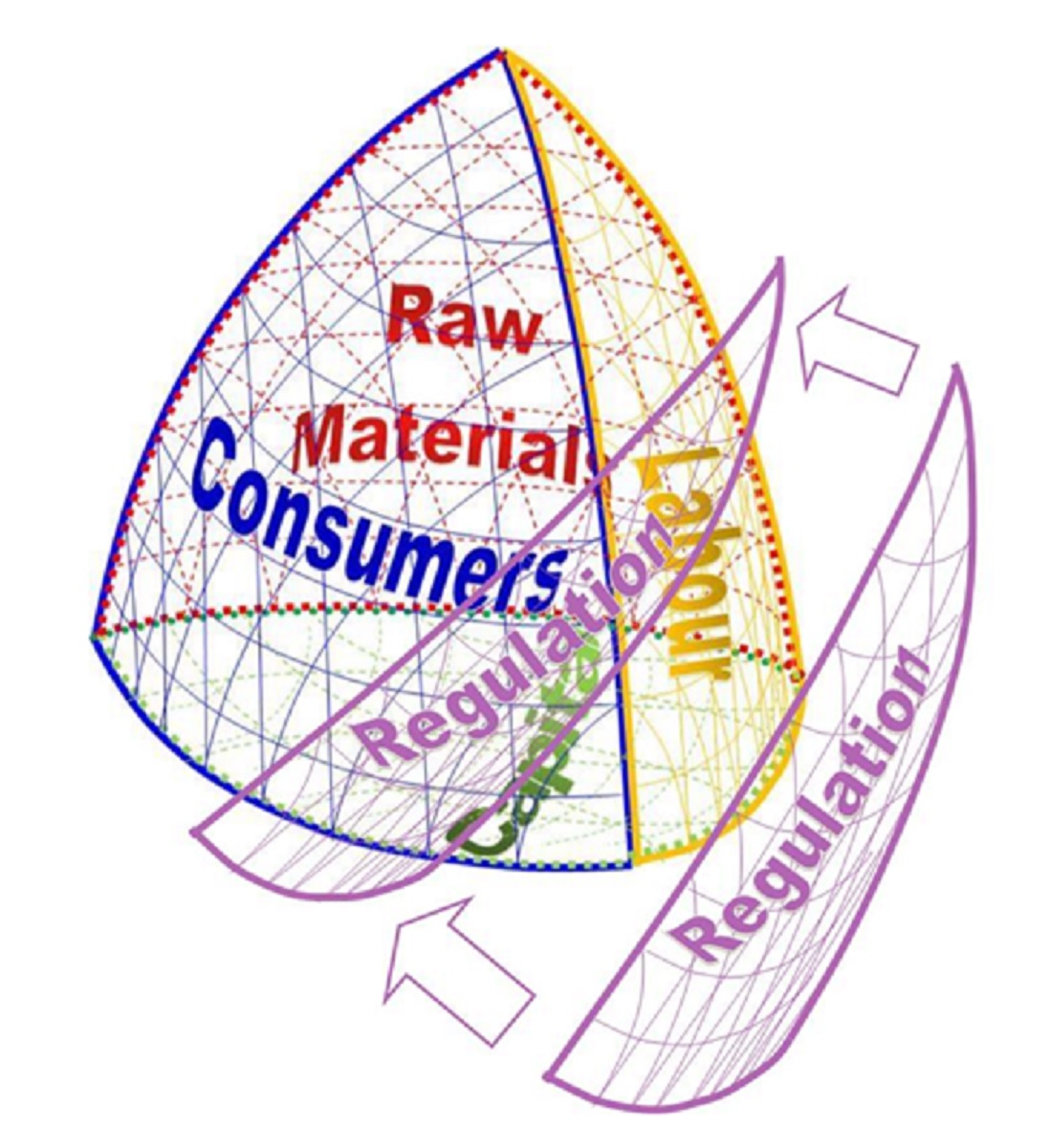

If a new external party intervenes, for example a government agency imposes regulation, the virtual space will be reduced correspondingly. Indeed, even the threat of regulation will have the effect of reducing the space as the firm is likely to take the view that it cannot afford to provoke the regulator.

Impact of new regulation to reduce solution space

So what is going on with ESG investment? ESG considerations have an impact on investment decisions in multiple ways.

Some investors will choose only to invest in businesses whose practices meet certain standards in terms of environmental and/or social responsibility and impact. When I was trustee of a large medical charity, we initially had a relatively limited list of sectors that we guided our fund managers to avoid, but progressively widened the list to avoid those whose products were implicated in contributing to the ill-health we working to address. Other charities have much wider exclusion lists, and many private individuals also choose to invest in ethical funds. Such investors are making an explicit trade-off between such potential increased returns as may be available from investing in companies (eg defence, tobacco) that don’t satisfy their ethical criteria.

Other investors decide to invest in ESG funds and businesses that meet ESG criteria because they believe that companies that with sound governance, ethical approaches to the communities in which they operate and setting high standards in their supply chains, and responsible approaches to the environment will ultimately deliver higher long term returns and be sustainable. Such investors may also take the view that these approaches also represent good business. Working in retail management as a merchandise director in the 1980s, I certainly took the view that being as environmentally responsible as possible was good business. I led a team that decided to adopt policies towards sourcing products from sustainable raw materials, reducing packaging, and developing “green” product ranges making extensive use of recycled materials on the basis that it was good for the business. It was good for our brand as it improved our standing with increasingly environmentally conscious customers. It was good for our sales, since people appeared keen to buy less environmentally harmful alternatives. It was also good for recruitment and retention of good staff, who seemed motivated (as I was) by working for a company that was trying to be environmentally responsible.

High standards of governance should also be appealing to investors, and the evidence is strong notwithstanding the mercurial successes of a few mavericks. As chair of a committee investing £200 million for the charity on which I was a trustee, I was attracted to Edinburgh based fund managers, Baillie Gifford, precisely because of the demands that it placed on the governance of their investee companies and its willingness to vote the shares it held for client like us to improve governance of the investee companies – and we were rewarded for our confidence in the approach by returns that consistently exceed the benchmarks for the fund.

If, as the flurry of FT articles suggests, there is an increasing appetite for ESG investing for whatever reason, the impact on companies is that (at least for the visually minded) the shape and precise orientation of their interface with the investment market will change reflecting either the trade-offs (in the case of the first type of investor described above) or the beliefs about the sustainability and long term returns (in the case of the second type of investor). The consequence of the appetite for ESG investing on companies is that those with business practices that align with the demands and expectations of ESG investors will face a slightly lower cost of capital and consequently increase the size of the solution space for the management teams when looking at their strategies.

John Tusa is an eminent former broadcaster, managing director of the BBC World Service, and managing director of the Barbican Centre. He is a veteran of a variety of boards of cultural organisations and proud of being described as possessing “the heart of a luvvie and the mind of a suit”. He has written an account of his experience of governance that should be on the reading list of everyone either occupying or contemplating appointment to a board. His experience may be drawn from not-for-profit organisations in arts, broadcasting and education, but it is as applicable to boards in the private and public sectors as it is to the third sector. As he remarks in the introduction to “On Board”[1]:

“It is sometimes assumed that boards in the business world are totally different from those in the not-for-profit sector. This is far less true than might first appear. Both kinds of board choose their chair and chief executive, both decide how they appoint colleagues, how they sell to or serve their public, their customers or their audiences; both are responsible for brand, communication and reputation; both supervise the internal health of the organization. Of course, one deals with profit, the other does not. But while ‘not for profits’ are not businesses, they must be ‘business-like in the way s they manage their resources.”

While Tusa does not have direct experience of private sector boards himself, he has sat on boards with plenty of people with this experience, notably Kenneth Dayton, founder of the Target retail chain in the US and Tusa’s chair at American Public Radio, who pointed out to him that “governance in the not-for-profit sector is absolutely identical to governance in the for-profit sector”, besides which that it can also be a lot more complex.

Tusa builds his account of governance around his experience on the boards of the National Portrait Gallery[2], American Public Radio, English National Opera[3], the British Musuem, English National Opera, Wigmore Hall, the University of the Arts London and the Clore Leadership Programme, each of which merit a chapter reflecting interviews with fellow board members, executives and other stakeholders. Tantalisingly, he also alludes to other experiences, such as his time as President of Wolfson College, Cambridge, but without the same detail. Most of these organisations faced major challenges during his time with them, some potentially threatening to their existence. His accounts of how the boards weathered their storms and his candour about the mistakes made along the way are pulled together with a short section ending each chapter drawing out his reflections on what he learned from each experience and provide a rich seam of learning not only for people joining boards for the first time but also for those with many board appointments already on the CV.

This book should be read for the lessons Tusa draws out at the end of each chapter. Board members would do well to reflect on each, and whether they are applicable to their organisations. But “On Board” can also be read for more: it provides anyone who has observed the ups and downs of some of Britain’s leading cultural institutions of what went on around the board room table. As someone with strong ties to the Isle of Portland, I was suitably scandalised by the failure twenty years ago to use Portland Stone for the Great Court development at the British Museum. Tusa’s first career was as journalist and tells a good story, about this debacle and much more besides, as well providing a required text for chairs, directors and trustees.

[2] His chair at NPG was Owen Chadwick, from whom I took my first lessons in chairing. Chadwick was Regius Professor of History at Cambridge University and a masterful chair of the faculty Joint Academic Committee, on which I sat as first year undergraduate (along with Diane Abbott, whose approach to faculty politics was considerably more radical than than the one she adopted later in her career as a leading member of the Labour Party in the House of Commons).

[3] I have a small gripe. John Tusa, having studied history at Cambridge, should know better than to suggest (in the context of ENO which, despite a catalogue of errors made by the board in the 1990s, managed to survive, an achievement that he observes “should not be underestimated”) that it was the French politician Talleyrand who said of his part in the French Revolution “I survived”. Far from just surviving, Talleyrand’s extraordinary achievement was to serve just about every government in France between 1780 and 1834, from the Ancien Regime, through every stage of the Revolution, the Napoleonic Empire, the Bourbon Restoration and the Orleanist “July Monarchy”. It was not Talleyrand, but Emmanuel-Joseph Sieyès, usually known as the abbé Sieyès, a chief political theorist of the French Revolution, who is reputed to have said in answer to a question about what he did during The Terror of 1793-94: “J’ai vécu”

The second session in the British Academy Future of the Corporation – Purpose Summit took place earlier this afternoon, with a focus on the role of stakeholders in purposeful business. The proposition in the Escondido Framework that what most people call stakeholders should be thought of as customers of the firm is at odds with conventional stakeholder theory, but for the purpose of this review I will talk about stakeholders as conventionally understood.

Some of the richest material in the session came from Victoria Hurth from the Judge Institute, although perhaps I reach this conclusion because the language she employs comes closest to that used in the Escondido Framework model of the firm. She framed her introduction to the session by talking about the relationship of corporate purpose to stakeholders being one in which the role of the market is to mediate the pressures from stakeholders. She also talked about tapping the wisdom of shareholders to give meaning to the purpose of the company, which may be another way of looking at the Escondido Framework view that the organisation exists to resolve the symbiotic needs of the stakeholders. She wrapped her introduction with an argument about need for diversity on boards to help with a paradigm shift away from a shareholder value driven model of the firm to one driven by purpose in the service of stakeholders – but without demonstrating the logic behind her argument. There may well be plenty of meat underlying her assertion, but today she did not have the time to make this part of her case.

Frances O’Grady, from the TUC, made the case for hearing the voice of the workforce on the boardroom, referring back to Theresa May’s proposals for changes to corporate governance and the subsequent review that I contributed to and commented on in 2016 and 2017. She explained that she is agnostic about whether worker representation should be in the context of a unitary board or a two tier board following the model in some northern European countries. She also argued for a change to directors’ duties, by implication beyond those set out in Section 172 of the Companies Act requiring them to take account of all stakeholders, to require more focus on the long term.

Dan Labbard, CEO of the Crown Estate (an organisation whose roots go back to 1066 and William the Conqueror) addressed the question of whether a focus on purpose creates additional risk to the corporation. He argued that a focus on purpose equips the corporation to recognise and then organise to address risk, in contrast to a primary focus on profit. He build on this argument by encouraging organisations to proactively go out to their stakeholders with a purpose led strategy, rather than merely responding to stakeholders, and to look at risk through a stakeholder perspective.

Jim Snabe chairs two of Europe’s biggest corporations, Siemens and Maersk. He framed his concerns around the impact on companies of globalisation, technological change and the climate crisis. He argued for leadership anchored in corporate purpose, which describes as explaining why your organisation exists. Leading two companies with two tier boards, he is an enthusiast for this model, explain that the “management board drives the bus” while the supervisory board “sets the GPS”. He sees four roles for the supervisory board: ensuring the strategy is correct by asking the right questions; ensuring that the strategy is aligned with the United Nations strategic development goals; promoting the next generation of leadership; and defining success in terms of addressing the needs of all stakeholders.

Colin Mayer opened the responses to questions by observing that it is difficult, notwithstanding the variety of means that can be considered (different board structures, consultative bodies, citizen juries), to capture the views of stakeholders. (for the Escondido Framework perspective, visit the section of this site addressing governance and some of the relevant earlier posts).

“This newspaper has welcomed the shift among corporate leaders from a narrow focus on shareholder value to the pursuit of a broader purpose — for a hard-headed reason: when business takes a broad perspective, it can leave everyone more prosperous, including shareholders. Rejecting the dogma of shareholder primacy is not a question of bleeding hearts, it is a matter of enlightened self-interest.” So says the FT editorial board in a powerful opinion piece today, before going on to argue that investors should follow suit.

The FT argues that there are two reasons for the investors to look beyond the bottom line and consider the impact of business decisions on climate and the environment and on workers and the communities they operate in. The first is that by ignoring the impending crises facing us, a corporate focus on shareholders alone contributes to the political neglect of the problems and can stand in the way of solutions. The second relates to the way that many investments are held by shareholders, through diversified portfolios intermediated by managed funds. The result of this is the ultimate investors (people like me with investment through pension funds, insurance policies and ISAs[1]) are in effect “universal investors” exposed to hundreds or thousands of individual companies, fortunes. As the FT team observe: “Their returns depend on that of the private sector overall. When one company profits by “externalising” its costs, that may flatter its bottom line only by losing investors more money in other companies which pay the price.”

Consequently, investors and company leaders both have an interest in internalising the externalities rather than ignoring them. But the FT finds that both company and investment managers feels constrained in doing so, and it argues that government should look at ways of changing the legal frameworks that shape behaviour by corporate leaders and fund managers.

My own belief is that there is evidence that some corporate leaders and some fund managers (notably Baillie Gifford who I got to know well over a period of nine years as the finance committee chair of an asset rich charity) do take the wider perspective and longer term into account and, in the UK at least, what is at issue is not so much the legal framework but the career paths, knowledge bases, incentive mechanisms, cultural biases and social norms in the City and in our board rooms.

[1] Individual Saving Accounts – the UK tax sheltered scheme for smaller retail investors

{kind=link}