It’s a bold step to claim to draw lessons from a war is that is not yet a month old, where the outcome is very far from clear, and the impact on the world in terms of economic disruption and political destabilisation way beyond the immediate geographic scope of the conflict.

This Russian invasion of Ukraine has so far been consistent with two of the great aphorisms about war. The failure of the Russian army in its assault on Kiev perfectly demonstrates that “no plan survives contact with the enemy”[1]. And the information coming from all sides, some understandable propaganda and disinformation, some amounting to exceptional self-deception, demonstrating the point originally made by Samuel Johnson in 1758[2] but later attributed in more pithy form to US politician Hiram Johnson in 1917 “the first casualty of war is truth”.

This war also demonstrates as well any other that existence of the three sanctions and the complex web of how they apply and interact. This is a war about the application of force and arms. It is also a war about the application of politics and persuasion. It is also a war where economic pressures are at work, where calculations about financial transactions and trade-offs are already having a huge impact.

The question is very reasonably asked how the European customers for Russian gas allow themselves to be propping up a Russian economy that Ukraine’s allies are trying to hobble through a trade embargo. Correspondingly, the world is being thrown into crisis by the impact of a shortage of Russian gas, whether held back by Russia to apply pressure on European countries or from a curtailing of imports driven by an act of policy. The impact on large parts of the world of restrictions of exports of grain from the Ukraine is likely to cause prices to rise in the affluent world and threaten famine in the less affluent.

At this stage, it is far too early even to speculate on the outcome. Will the wave of political sympathy in the West and suspicion of Russia’s motives among the former colonies of both Soviet and Tsarist empires outweigh the economic pressures that may undermine the popular support for the Ukrainians? Will the costs and potential duration of the “special military operation” undermine the political support for Putin’s irridentist claims? How does the Chinese claim on Taiwan play into the political and economic debate and super power balance?

Playing into the corporate world that is the home turf of the Escondido Framework, companies have to take into account the changes to the pressures that they work under. The virtual spaces between market interfaces within which they operate will change. This will reflect changing patterns of supply and demand for resources and for their outputs. It will also reflect changing patterns of government interference in the shape of the restrictions on where they source and where they sell. It will introduce uncertainties where previously there may have seemed a degree of foreseeability. And all this following on the heels of the pandemic and in the context of a climate crisis.

[1] “One cannot be at all sure that any operational plan will survive the contact with the main body of the enemy” Herman von Moltke in “On Strategy”

[2] “Among the calamities of war may be jointly numbered the diminution of the love of truth, by the falsehoods which interest dictates and credulity encourages” Samuel Johnson in “The Idler” 1758

During lockdown, Declan Donnellan and Nick Ormerod, artistic directors of Cheek by Jowl[1] recorded a weekly podcast “Not True but Useful” about their approach to working in the theatre. They have now released transcripts of the first series of stimulating conversations. The following is an extract from the second of these podcasts “Space and Shakespeare”, published in April 2020[2]. I reproduce it here because I find the visualisation of the firm and the organisation as something existing in space, bounded by its interfaces (which are themselves dynamic) with outside world very helpful when thinking about the firm, what it is there for, and how people interacting with the firm or setting its strategy from inside. Listening to Declan and Nick in conversation with interviewer Lucie Dawkins, I was struck by parallels between what happens to actors on stage and to the managers of the firm.

Lucie So, today we’re going to focus on the way that you think about space when you stage your plays together, both in terms of what it means for the actors, and how it influences your design. And later in the episode, we’re going to use Measure for Measure as a test case, and I suspect we’ll probably talk a bit about Macbeth as we go along. But let’s start at the very beginning. Why is space so important to you?

Declan It’s very difficult to explain what we mean by space. I can put it in this form, I can say that what happens when we die? When we die, the space gets taken away from us. So the space is an enormous thing.

Lucie So what has space got to do with acting?

Declan Everything. It’s got to do with our whole existence.

Nick Human beings live in space. They’ve spent their lives dealing with the space, they are formed by the space, everything. The character (Macbeth, for example) lives in a space, achanging space from second to second. Each character has their own special space. And it’s very subjective. You look at a chair, perhaps your mother sat in that chair, that chair means something to you in your bedroom. The character deals with the space. And we as human beings spend our lives dealing with a space.

Declan Yes, sometimes it’s a criticism, a lot of people say, oh, you know, ‘he’s at the centre of the universe. He thinks he’s the centre of the universe.’ And of course, it’s very annoying if somebody’s self-obsessed like that. But unfortunately, we are at the centre of our own universes. We invent the world that we see. There is a reality, I’m sure, but we have no access to that reality other than through our imaginations. Nick and I are looking at a microphone now but we’ll see different microphones. The microphones we see we have to invent somehow in our heads. One can’t explain these things, but we can get used to these ideas. And we can say things about the space, which is different from defining it.

Lucie How does the space influence the behaviour of a character, for example?

Declan Well, there would be no character if there were no space. And the thing is that, in a mysterious way, we are not independent of the space, we only exist as part of this big binary. And that’s the very hard thing to get one’s head around.

Lucie That’s a striking statement, that there’s no character without the space around them. So, let’s unpack that a bit. How, for example, does the space define Macbeth in the scene we talked about last week, Act 1 Scene 7, when he leaves the dinner party in the next room offstage to talk to the audience about why he wants to kill Duncan.

Declan I think that first we shouldn’t in any way have the idea that space is something that only afflicts Shakespearean characters. You know, Nick and I are sort of hunched over a microphone and we’re looking at your face, and we’ve the laptop open, and I’m trying to not make noise on the table. And I’m pinned in space.

For Macbeth, there’s a million different ways of doing it, but the space will be central to all of them. There is no world, there’s no life beyond the space. The space is what gets taken away from us when we die, and death is what happens when the space gets taken away. Macbeth gets the feeling that he has to leave that table. Yes, we can interpret the stakes: because he feels suffocated; because there’s no air in the room; because he has to get away from the man he is murdering; he needs space to think – and he comes out, and maybe doesn’t want to speak to anybody, and maybe he sees us, and there are all sorts of stories that one might evolve in order for him to do that. But whatever solutions he comes up with, these will all be absolutely dependent on the space, and on him allowing that space to come before he does. That is the important thing. So it’s not me and I spray a space around me – it’s that is a space and I’m in it. I try to control that space. And so I imagine it to be all sorts of things other than it is. But it’s going to be there before me, during me, and after me, and my perception of it will be continually changing.

If we need to break it down into steps, we can say – it’s a bit leaden – but if we run into difficulty, we can say that one of the shapes of life is that I’m in a space, I have an impulse to cross a threshold to go to another space to find something which turns out to be different from what I had expected. And that last one gives us life, the fact that it’s a continual surprise. When we look at any space, we see it’s just one long transition from one space to another. There is no state of a space, the space itself is transitioning, and we are normally trying to keep up with that space that’s changing much faster than is comfortable for us. It’s like, you know, we think that the world is spinning too slowly. Actually it’s spinning uncomfortably fast. And in all of these plays, events run out of control, and that they’re trying to slow things down. It’s rather sad to say to actors, you know, you must drive the play, because actually the space, the thresholds, the predicament, drives the action. And the characters are struggling to keep running with this thing that’s running wild and out of control.

Lucie So, one way of looking at what’s driving this character through the space is that there’s a problem in one space, it drives them into another space, but the new space only keeps presenting him with more problems – that the character’s journey through the scene is dealing with the problems that the space is serving up to them.

Declan That’s exactly right. Yes, the space is never what he wants it to be. The space keeps presenting new challenges. And we all think, oh wait, if only the threshold changing would stop, if only the carousel would stop, then I can deal with it – if only it would stop! But itdoesn’t. It just keeps going. And there we are. And that’s what we do. And yes, he’s continually dealing with the new things that he sees.

Lucie So it sounds like the space is never static because the problem keeps changing all the time. I guess the longer he’s out of dinner, the more he realises that he’s going to be missed, and it looks suspicious, and the bigger his problems keep getting, and every face that he speaks to in the audience presents another source of discomfort, as if he’s trying to persuade each one that the murder is a great idea. So the space is always changing, either serving up new problems or letting the existing ones grow worse.

[1] I have been one of Cheek by Jowl’s patrons for many years, having enjoyed their shows for most of my adult life and almost certainly seen performances involving Declan and Nick in my first year at student at Cambridge University in the 1970s.

As someone with an advisory role and financial interest in just such a business for the past ten years, the explanation provided by Apple’s CEO, Tim Cook, has a hollow ring:

“Small businesses are the backbone of our global economy and the beating heart of innovation and opportunity in communities around the world. We’re launching this program to help small business owners write the next chapter of creativity and prosperity on the App Store, and to build the kind of quality apps our customers love. The App Store has been an engine of economic growth like none other, creating millions of new jobs and a pathway to entrepreneurship accessible to anyone with a great idea. Our new program carries that progress forward — helping developers fund their small businesses, take risks on new ideas, expand their teams, and continue to make apps that enrich people’s lives.”

The suggestion that this is a natural evolution and being done out of the goodness of Apple’s corporate heart is implausible at best. The small businesses that rely on the App Store to reach iPhone customer have been “the backbone of the global economy and beating heart of innovation and opportunity” throughout the iPhone’s existence and have put up with being fleeced. The entrepreneurs have funded their businesses, taken risks on new ideas, expanded their teams and made apps that enrich people’s lives without any help from the black shirts* formerly of Infinity Loop, now Apple Park.

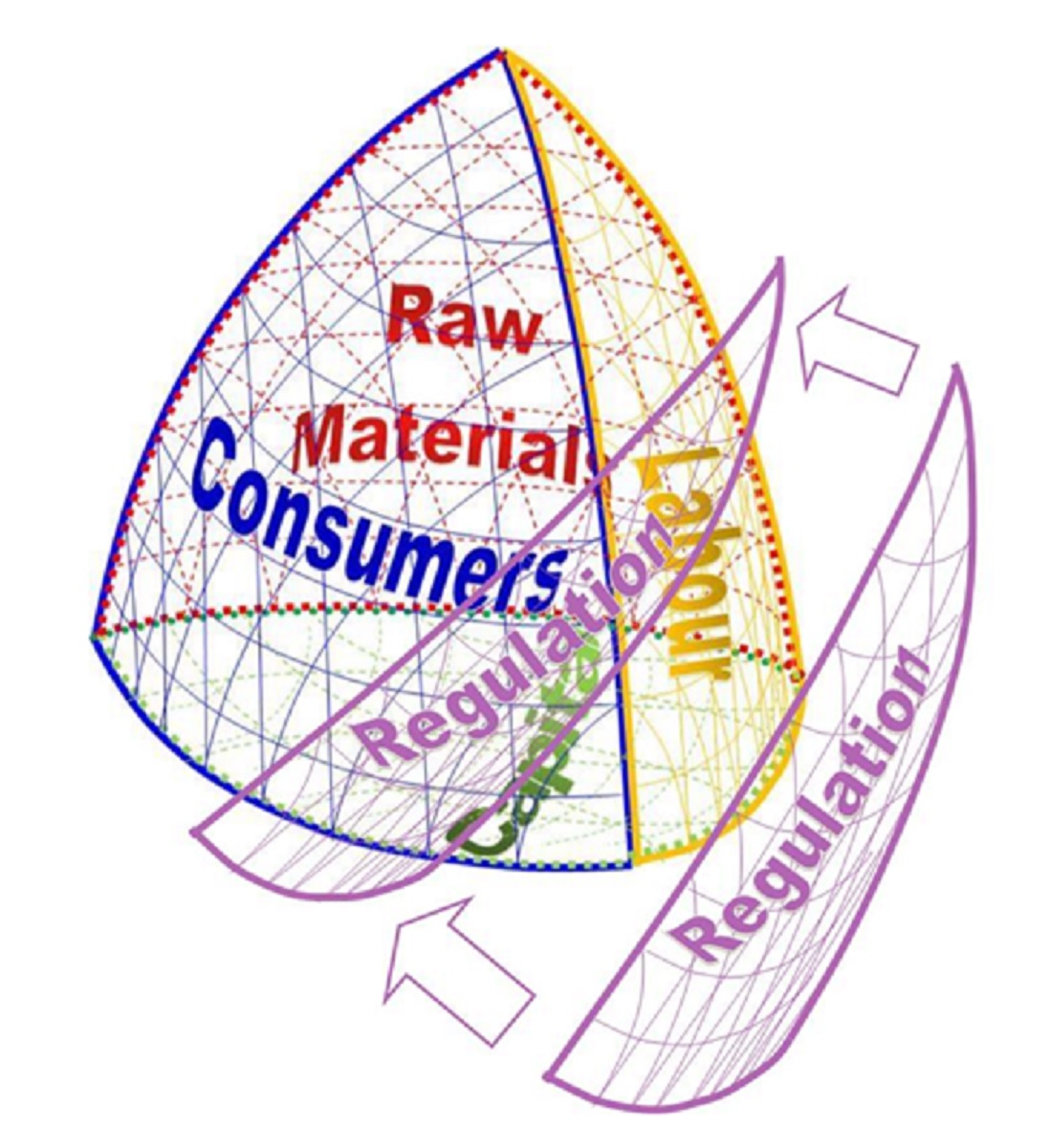

The likely explanation is provided by the threat of action from the European Commission, which opened an investigation into Apple’s anti-competitive behaviour in June, and potentially from the US, with Congressional hearings into the monopolistic conduct of the tech giants later in the summer. This is an illustration of the strategic solution space available to a company being reduced by the prospect of regulatory intervention.

In parallel with this reduction in the price charged to its small customers for using the App Store, Apple revealed at the Congressional hearings something about the shape of the market interface between the App Store and the “customers” who sell through it when it disclosed that it had agreed a 15% commission with Amazon for in-app charges within the Prime Video app.

The interesting question is what happens next. Apple has had to cave in to the threat of another web behemoth flexing its market power and potential to lobby against it. It has accepted, so far in part only with the new deal for smaller developers, the political reality of the forces gathering against its abuse of its power over a large slice of the market for apps on mobile phones. What of the middle-sized App Store developer customers? How long will it take Apple to develop an implausible but face-saving formulation to explain why it has reduced their commissions too? Or will it try to tough it out until competition authorities around the world run out of patience and take Apple, and potentially some of the other tech giants, apart in the way they did to the US rail and oil industry over a century ago?

* for the avoidance of doubt, this is a reference to the sartorial style of the late Steve Jobs and his successors and not a comment on either their conduct or politics.

What better illustration could there be of the Escondido Framework approach to understanding ESG investing described in last week’s blog than the defenestration of Rio Tinto’s chief executive, Jean-Sebastien Jacques, by the company’s shareholders?[1]

In relation to the distinction made in last week’s article between the impact of regulation on the solution space available to executive teams, one of the interesting aspects of the dynamiting of Juukan Gorge and the two rock shelters is that the company had previously negotiated native title agreements with the Puutu Kunti Kurrama and Pinikura people, giving it rights to mine the area and had also secured regulatory approval. In Escondido Framework terms, as illustrated in last week’s blog post, the company thought that it was operating within the solution space defined by the market transaction with the owners of the land and that the regulatory market interface had not reduced the solution space available to the company.

However, the executives had failed to appreciate the sensitivities of the company’s investors to such an egregious violation of the heritage of not only the indigenous population but humankind as a whole.

Perhaps the board and executive team at Rio Tinto paid too much attention to the likelihood that investors in mining stocks are already a self-selected group that is less sensitive to ESG considerations than the investment market overall.

It matters little whether the response of the investors whose pressure on the board finally persuaded chairman Simon Thompson (who previously had insisted that Rio Tinto would not fire Mr Jacques) was a reflection of the potential for the scandal to increase future regulatory pressure on the industry, or a concern for the response of the upstream investors in their funds, or the consciences of fund management executives themselves being pricked by comparisons between the dynamiting of the caves with the actions of the Taliban blowing up the Bamyam Buddhas in 2001.

Either way, the shape of the investment market interface was sufficiently different to that perceived by Mr Jacques and his colleagues for them to have placed themselves, not temporarily but at a personal level permanently, outside the solution space available to them.

[1]For anyone who missed the story, Rio Tinto blew up two 46,000-year-old Aboriginal rock shelters in Western Australia, offending not only the Australia aboriginal community for whom the sites were sacred but also a wider public sensitive to an ancient archeological heritage. Initially the board decided to withhold bonuses for the executives involved, but has now decided that Mr Jacques should go (albeit not until early next year and without any further financial penalties)

The Financial Times has published a flurry of articles and the occasional letter about ESG (Environmental, Social and Governance) investing recently.

For example, Geeta Aiyer, president of Boston Common Asset Management, was the subject of a profile on 29th August. This followed the success of Boston Common and other investors to secure the change of name of the Washington Red Skins American Football team by applying pressure on FedEx, the logistics company which sponsors the team’s stadium.

On 1st September the paper published an article about write-downs at BP and Shell in response to “scores of asset managers who have doggedly pressed the oil companies to set targets to reduce carbon emissions and recognise the financial impact climate change could have on their operations” . The article cites a number of leading fund managers who comment on the “explosion” in ESG investing. It also notes the role of regulation in changing perspectives, citing the requirement now placed on pension fund managers in the UK take sustainability issues into account in their investment decisions and the impact of the EU’s sustainable finance package which will, from March 2021, push asset managers to incorporate ESG risks in their decision making.

A day later, on 2nd September, the FT published an article by Chuku Umuna, former Labour business spokesman and now lead for ESG with Edelman, the public relations consultancy, arguing that “a company’s ability to manage ESG factors is widely viewed as a proxy for prudent risk management, and with good reason”, citing work by Société Générale on the impact of ESG-related controversies that found that “in two-thirds of cases a company’s stock experienced sustained underperformance, trailing peers over the course of the following two years.”

A few months earlier, on 9th July, Gillian Tett wrote an article that opened by observing that the major ESG indices in the US and in Asia had outperformed the equivalent all share indices in terms of the financial returns to shareholders and cited a report from BlackRock making the same case, not only in the past year but also in 2015/16 and in 2018. BlackRock put this down to two primary reasons: the momentum created by ESG investors pushing up prices as they seek to acquire these stock for their clients and beneficiaries; and the value to companies seeking to improve their ESG ratings the scrutiny to which they subject their supply chains and employee practices and the consequent benefits that arise to their businesses.

Does the Escondido Framework approach to understanding organisations help us understand what is going on?

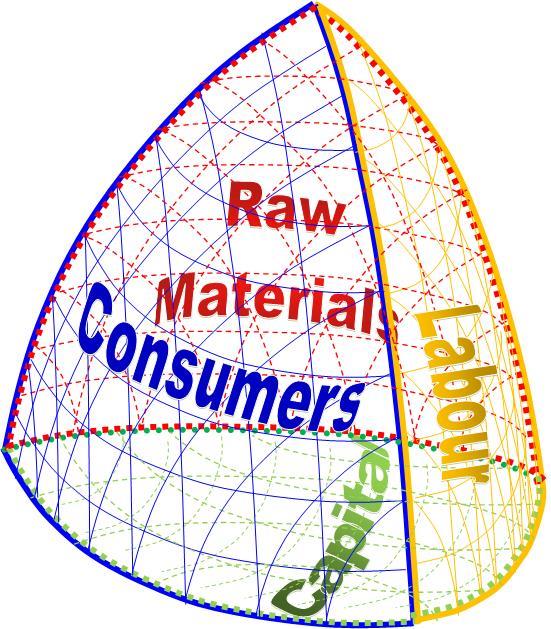

The Escondido Framework approach to looking at the firm is described in detail elsewhere. In essence, it explains that firms exist as a virtual space defined by their market interface with the suppliers of capital, labour, suppliers of goods and services, and customers, plus others whose needs may need to be satisfied, such as government or the wider community who implicitly or explicitly provide the firm with a license to do business. Their survival depends on creating value through the efficiency of their internal operations for there to be such a space. Where the firm places itself within the space will determine the distribution of economic rent to the stakeholders, how much may retained by the executive management, and how is available for reinvestment either in assets or long term relationships with one of more sets of stakeholders. As the market interfaces changes – through changes in supply and demand, competition, or the trade-offs made by the other parties to the markets place exchange – the virtual space (which can also be considered as the solution space available to the management team) may expand or contract (increasing or reducing the range of options, strategies and potential profitability available).

If a new external party intervenes, for example a government agency imposes regulation, the virtual space will be reduced correspondingly. Indeed, even the threat of regulation will have the effect of reducing the space as the firm is likely to take the view that it cannot afford to provoke the regulator.

Impact of new regulation to reduce solution space

So what is going on with ESG investment? ESG considerations have an impact on investment decisions in multiple ways.

Some investors will choose only to invest in businesses whose practices meet certain standards in terms of environmental and/or social responsibility and impact. When I was trustee of a large medical charity, we initially had a relatively limited list of sectors that we guided our fund managers to avoid, but progressively widened the list to avoid those whose products were implicated in contributing to the ill-health we working to address. Other charities have much wider exclusion lists, and many private individuals also choose to invest in ethical funds. Such investors are making an explicit trade-off between such potential increased returns as may be available from investing in companies (eg defence, tobacco) that don’t satisfy their ethical criteria.

Other investors decide to invest in ESG funds and businesses that meet ESG criteria because they believe that companies that with sound governance, ethical approaches to the communities in which they operate and setting high standards in their supply chains, and responsible approaches to the environment will ultimately deliver higher long term returns and be sustainable. Such investors may also take the view that these approaches also represent good business. Working in retail management as a merchandise director in the 1980s, I certainly took the view that being as environmentally responsible as possible was good business. I led a team that decided to adopt policies towards sourcing products from sustainable raw materials, reducing packaging, and developing “green” product ranges making extensive use of recycled materials on the basis that it was good for the business. It was good for our brand as it improved our standing with increasingly environmentally conscious customers. It was good for our sales, since people appeared keen to buy less environmentally harmful alternatives. It was also good for recruitment and retention of good staff, who seemed motivated (as I was) by working for a company that was trying to be environmentally responsible.

High standards of governance should also be appealing to investors, and the evidence is strong notwithstanding the mercurial successes of a few mavericks. As chair of a committee investing £200 million for the charity on which I was a trustee, I was attracted to Edinburgh based fund managers, Baillie Gifford, precisely because of the demands that it placed on the governance of their investee companies and its willingness to vote the shares it held for client like us to improve governance of the investee companies – and we were rewarded for our confidence in the approach by returns that consistently exceed the benchmarks for the fund.

If, as the flurry of FT articles suggests, there is an increasing appetite for ESG investing for whatever reason, the impact on companies is that (at least for the visually minded) the shape and precise orientation of their interface with the investment market will change reflecting either the trade-offs (in the case of the first type of investor described above) or the beliefs about the sustainability and long term returns (in the case of the second type of investor). The consequence of the appetite for ESG investing on companies is that those with business practices that align with the demands and expectations of ESG investors will face a slightly lower cost of capital and consequently increase the size of the solution space for the management teams when looking at their strategies.

I attended the launch of “Collaboration Strategy: How to Get What You Want from Employees, Suppliers and Business Partners”, the new book by Felix Barber and Michael Goold of the Ashridge Strategy Management Centre. The book contains plenty of good material on structuring terms with the parties who you work with and aligning incentives. Reflecting the past service of both authors with the Boston Consulting Group, it has plenty to say about focusing on those activities in which you enjoy competitive advantage and outsourcing the others.

Publisher’s glass in hand, I was listening to Felix deliver a short lecture providing a synopsis of the themes of the book when someone¹ muttered in my ear: “they’re talking entirely about markets and financial incentives, but in reality it’s 80% Dark Matter”. This is a powerful metaphor and an important insight: we need to recognise that there is lot of dark matter out there in the economy and without it nothing works. Market forces and financial incentives alone do not explain how organisations, partnerships and collaborations operate and why we need them. Barber and Goold do acknowledge, buried deep in their text, that there may be more going on by commenting that they “don’t wish to downplay the importance of other approaches to motivating employees and other partners”. But, possibly reflecting lifetimes as consultants and academics, they convey in the book the impression that they don’t recognise the amount of Dark Matter that the system needs.

¹ David Pitt Watson, sometime managing director of BCG rivals Braxton Associates, Labour Party Finance Director, boss of the activist investment fund Hermes Focus and now social entrepreneur and responsible investment guru.

The Escondido Framework starts from the assumption that the company (in common with many other forms of organisation) is defined by its interfaces with the various market places in which it operates, in the simplest form the markets for labour, raw materials, capital and finished goods or services. These are, in effect, its boundaries. And while there are differences between markets, in essence they all reflect an exchange between two parties for mutual benefit – the employee receives payment and other non-financial rewards for his labour; the supplier of raw materials payment for the goods provided; the supplier of funds either interest or dividends and the prospect of capital growth for forgoing use of those funds for his own short term benefit; and the customer goods or services in exchange for payment. The Framework also reflects the view that being a party to the exchange does not of itself mean that the other party has a “stake” in the company or “own” it in any absolute sense. There may be a contractual relationship between the party and the company which reflects the terms of the exchange and provides structure for enforcement but essentially this is a mutually beneficial relationship in which both parties have duties to deliver their side of the bargain.

Within the Framework, there is no assumption that any of the providers to the company – of labour, raw materials, capital or revenue – any superior rights or claims over the company, in traditional parlance, “ownership”. Legal devices may be put in place by the state, or may exist in the form of contractual agreements that provide these other parties with rights, for example: in the form of wages and employment rights; to payment for goods at a particular point in time; to payment of interest or dividends; and to return of capital under prescribed terms and with differing degrees of confidence. The contracts and legal frameworks may also define mechanisms under which these other parties may enforce these rights, but enforcement is also be a function of other considerations that reflect market conditions rather than the law, for example: what alternatives are available to a workforce with a specific set of skills and ties to a particular geography; what other customers are available for the raw materials, and how much are they willing to pay; what will other prospective providers of capital pay for these shares or bonds, and how easily can we replace the existing board and executive team; and how often do customers in consumer markets consider, let alone read terms and conditions.

The Framework suggests that the company can be considered as a “virtual space”, existing between these market interfaces. The location and shape of each of the market interfaces reflects what economists think of as the demand function and marketing academics describe as indifference curves, i.e. how customers make trade-offs between the various attributes of a product. These are also shaped by the competition that the company faces: when recruiting from a limited pool of skilled employees; for sourcing scarce raw materials; seeking funding from a limited capital market, or seeking the custom of consumers who can buy from other companies or who may be able to substitute one item for other goods. Remove the competition and the market interface or boundary moves outwards, increasing the volume of the “virtual space” available to the company. Improve the operating efficiency within the company or secure a competitive advantage over other participants in one of the markets concerned and the volume of the “virtual space” will also increase.

At any particular point in time, for any particular product or service it sells, these interfaces will be brought together, or resolved, at a single virtual point at which of each of the providers is rewarded at prices that are, all things considered, satisfactory to them. In perfect market equilibrium, all prices would be at market clearing levels, no-one would realise economic rents, and there would one point at which the interfaces would be resolved. No self-respecting economist has ever viewed the perfect market paradigm as anything other than a useful benchmark for understanding a world which is dynamic and virtually always distant from the paradigm, and in this the Escondido Framework is no different. In reality, the “virtual space” is just that, an available set of points at which the price levels may be resolved. Depending on the scale of the external market failures that allow for the internal organisation of economic activity to generate greater efficiency, there is potential for the management of the company to elect where to set prices and where on the indifference curves to locate the marketing proposition to each of the other parties (suppliers or labour, raw material, capital and custom), and how to allocate the economic surplus that the absolute volume of the “virtual space” represents.

{kind=link}

{kind=link}