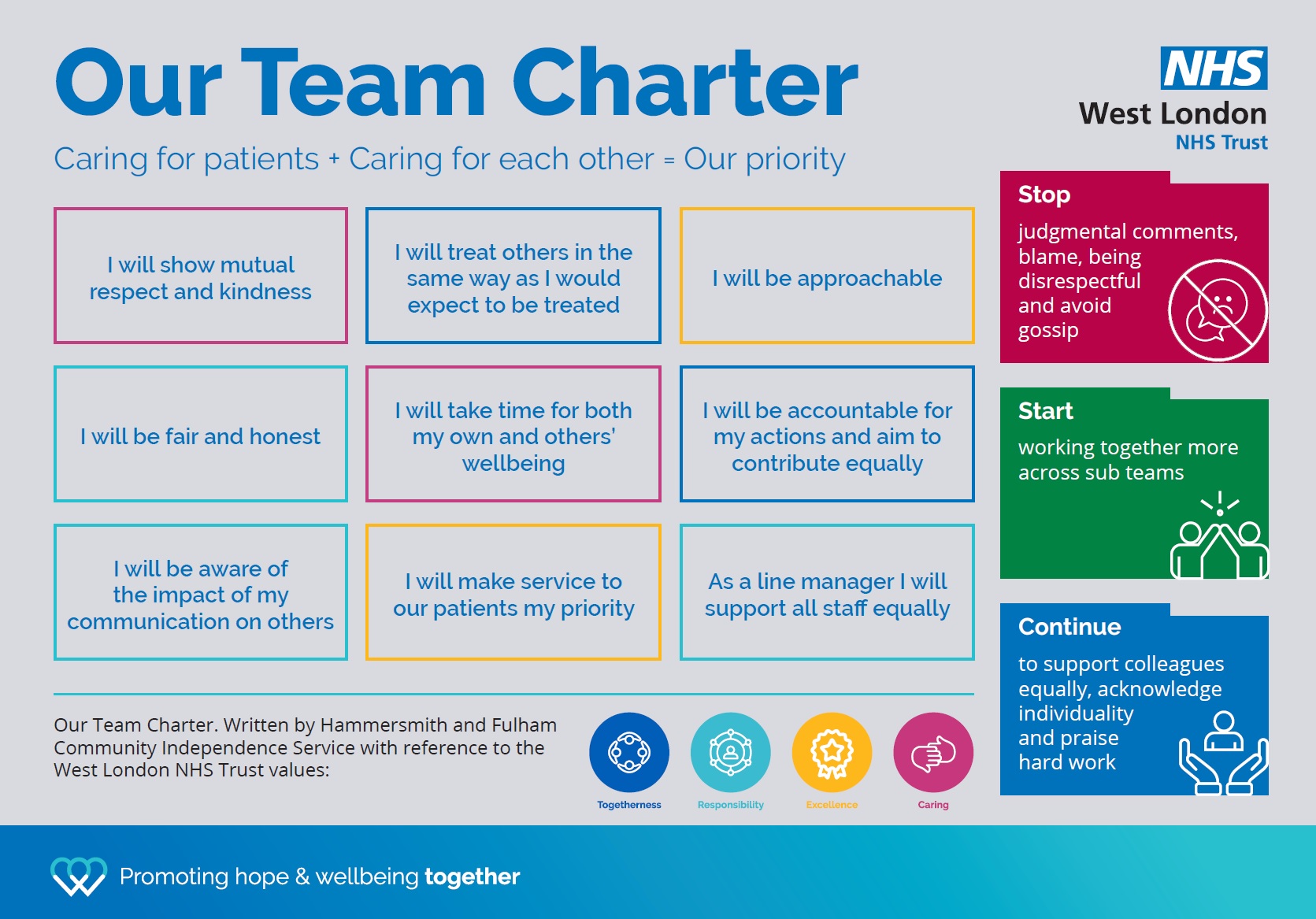

I couldn’t fail to be impressed by a slide in a recent presentation by the community health director at the NHS Trust that I have chaired for the past eight years. It described the Team Charter developed in a programme of mutually agreed behaviour workshops in the Hammersmith & Fulham Community Independence Service in which community nurses, occupational therapists, physiotherapists, and care workers support patients to keep them out of hospital. They are a high performing team delivering a great service, facing challenging demands, working with constrained resources, juggling priorities, and taking difficult decisions. The Team Charter illustrated above speaks for itself. It may look like a “motherhood and apple pie” recipe, but it is no worse for that. And, what’s more, it provides a lesson for teams and their leaders everywhere.

A “Big Read” feature in the Financial Times recently (23rd February 2023) described how the isolation of Vladimir Putin within the Kremlin and narrowness of the circle he consults contributed to his disastrous decision to invade Ukraine and subsequent conduct of the “special military operation”. Pictures can paint many thousands of words, but if there was anything to illustrate the need for the Kremlin to take a lesson from the healthcare workers of Hammersmith & Fulham, the photograph below, used by the FT to accompany its article, does the job.

Putin with foreign minister Sergei Lavrov – would they benefit from a team charter?

Chartists meet on Kennington Common in 1848 – the year of the Communist Manifesto and “All things bright and beautiful”

I went into the first Covid-19 lockdown in March with three doorstep sized volumes to keep me going.

The 912 pages of Hilary Mantel’s Mirror and the Light were riveting, even if I knew from the outset that Thomas Cromwell’s career would come to an abrupt end at Tower Hill in 1540. The 1088 pages of David Abulafia’s magisterial The Boundless Sea kept me entertained as it opened my eyes, chapter by chapter, to the way that different parts of the world became progressively connected by maritime exploration, communication and trade.

I had started turning the 1041 pages of Thomas Piketty’s Capital and Ideology before restrictions started to be lifted in May but, despite finding some stimulating ideas in his opening account of the different sources of power of different parts of premodern society (which he describes as ternary or trifunctional, and have echoes in the Escondido Framework’s account of the three currencies or sanctions), it was not until the re-imposition of lockdown (the UK government’s Tier 4 restrictions) that I finally completed it.

I admire much of what Piketty has done in Capital and Ideology. His effort to document the movements in the shares of income and wealth between different groups in different societies throughout human history, and particularly the past century or so, is admirable and revealing. It is possible to challenge some of his assumptions and definitions, but the picture he paints of the direction of the trends in material inequality are compelling. I agree with his spin on Rawls’s maximin principle: “To the extent that income and wealth inequalities are the result of different aspirations and distinct life choices or permit improvement in the standards of living and expansion of the opportunities available to the disadvantaged, they may be considered just.” (p.968). His chapters on the increasing support of the “Brahmin” classes educated to degree level for parties of the left and the corresponding “Nativist” alignment of parties of the traditional right and “left-behind” communities are persuasive. But the book is far longer than it needs to be, many of its graphs add little, and he strays from the professorial scholarship of the economist/social scientist-turned-historian into an undergraduate level of prescription.

Piketty’s underlying thesis is that “no human society can live without an ideology can live without an ideology to make sense of its inequalities.” I didn’t need to read 1041 pages to recognise this: growing up in a churchgoing family, I remember singing the third verse of “All Things Bright and Beautiful”

The rich man in his castle,

The poor man at his gate,

God made them, high and lowly,

And ordered their estate.

These days, it is generally omitted!

It may or not be a coincidence that Mrs Cecil F Alexander wrote these words in 1848, the “Year of Revolutions”, in which Marx and Engels also wrote The Communist Manifesto. Piketty chooses to reformulate the opening words of its first chapter “The history of all hitherto existing society is the history of class struggles” as “The history of all hitherto existing society is the history of the struggle of ideologies and the quest for justice.”

There is something in Piketty’s thesis about the relationship between the ideas that prevail at any point in time and the organisation of society and its impact on the distribution of wealth and income. It may be that I started out as a historian whereas has come to history by way of economics, but I find that he oversimplifies to sustain his argument. Ideas ebb and flow and they can influence behaviours, but this is not the same thing as saying that they determine behaviours. He falls into the trap of assuming that the behaviours that are generally ascribed to “capitalism” are the product of the past few centuries.

He frequently quotes Karl Polanyi with approval, who was even more blinkered in this respect, regarding capitalism as an entirely modern phenomenon. Peter Acton has undermined Moses Finlay’s thesis that the ancient economy was shaped by considerations of status and civic ideology rather than rational economic considerations, demonstrating in Poiesis: Manufacturing in Classical Athens demonstrates that the commercial decisions of Athenians “were for the most part…consistent with today’s understanding of good (rational, profit-maximising) business practice[1]. It does not require a 21st century reading of the biblical parable of the talents to see that the notion of investing for a return was established by the time the Christian gospels were written. And Abulafia’s The Boundless Sea, contains plenty of evidence for the commercial underpinning of the development of maritime trade over many centuries. One of the primary shortcomings in Polanyi’s approach was that set very specific conditions around anything that he would define as a market and, by framing his argument in this way, created a platform for his dismissal of the longstanding heritage of commercial activity. It is as though Polanyi, and to a lesser extent Piketty, seek to dismiss market mechanisms and their place in human societies on the basis that, prior to Adam Smith and his successor, the conditions assumed in classical economics had neither been articulated nor did they prevail.

Essentially, it is not that Piketty is wrong, but his case is overstated and needs reframing. It is not that ideology determines the form of economic organisation, but it helps shape relationship between the parties. In Escondido Framework terms, the prevailing ideological frameworks will influence the attitudes and trade-offs made by parties in their relationships with each other at market interfaces. For example, a religious ordained prohibition on usury does not undermine the human behavioural drivers for gratification today over gratification tomorrow and discounting for risk (although these can be culturally influenced), but historically has resulted in work-arounds (eg Islamic finance) or lending being undertaken by a community less constrained by the prohibition. Certain activities, as in caste based societies, may be undertaken by tightly defined social groups, with implications for the commercial terms on which these activities take place. But this is not the preserve of caste societies: while the boundaries may be less clearly defined and not religiously ordained, even in contemporary society there is an intergenerational stickiness in occupations and values, traditions and attitudes acquired in childhood shape occupational choices and behaviours.

So, two cheers for Picketty for the underlying thesis. And, in due recognition of his own disclaimer in his concluding chapters, he has set out to provoke further debate and provide the foundation for further scholarship rather than provide the definitive answer

However, where I find Capital and Ideology most flawed in when Piketty moves from diagnosis to prescription. In particular, his leap from describing to the increasing inequality in economic outcome for the richest few percent compared to the poorer mass of the population to concluding that all would be solved by appointing worker representatives to corporate boards highlights the danger of straying too far from your own area of expertise.

The inequality that Piketty documents arises from the endowments that we start out with in life (geography, genetics, family wealth, upbringing, education) and our life choices and chances (too many possibilities to enumerate). These will shape whether we end up with investable wealth (the impact of this on equality is thoroughly documented in his earlier work: Capital in the 21st Century) and whether we end up in positions in which we have market power and are able to extract economic rent, which has arisen most egregiously in recent years for executive directors of large companies as a result of shortcomings in corporate governance. Addressing inequality arising from our endowments needs primarily to be by “levelling up” in terms of investment in education and social support, particularly in early years, and widening opportunities, but in relation to inherited wealth is a proper area for taxation. Addressing inequality arising from investable wealth is also clearly an issue for taxation and also needs international solutions, but is a complex matter not least because of the risk of creating perverse incentives and unintended outcomes. Taxation has its place in addressing inequalities in income, but as with addressing issues surrounding taxation of wealth and wealth transfer, is also fraught with difficulty. Piketty raises these issues quite correctly.

But addressing inequality arising from market power and the ability to extract economic rent is a proper matter for better corporate governance and regulation to address market failure. Piketty fails to recognise the role of market failure and consequently the need to address this, and also the problem of the increasing ability of corporate management (and some of the services that support them), to extract economic rent (ironically, at least in part, at the expense of the owners of investible wealth), and that this is purpose behind the need for reform of corporate governance. His own prescription, worker representation on boards, is not the solution for reasons that I have argued elsewhere. Rather, and this comes back to his underlying thesis around ideology, there is a need to widen the understanding about the proper purpose of the company (the core of the Escondido Framework), and an improved understanding of the role of boards in serving them.

[1] Acton P (2014) Poiesis: Manufacturing in Classical Athens. New York: Oxford University Press

Rousseau observed that “Man is born free but everywhere is in chains”. Many people in business, politics and media talk about markets in a similar way, as though “free markets” are the natural state and desirable order and any intervention by an agency of the state or collective popular action is represents an undesirable fettering of enterprise.

Economists since Adam Smith have recognised that markets can fail and may need to be subject to intervention. Even figures as inspiring to simplistic supporters of free markets as Milton Friedman recognise that there are proper roles for the state where markets fail.

Diane Coyle starts in much the same place as other economists who look at limits of markets and the place of government intervention in markets. She starts with conventional analysis of market failures, listing seven instances of failure in the conditions required for free markets to be efficient. She returns these seven types of failure throughout her examination of the relationship between markets, the state and people, and description of the appropriateness of state intervention or collective action to address.

In cataloguing the failures and the responses to them, Coyle assists the reader, from the economics or politics undergraduate or MBA student getting their first exposure to welfare economics and public policy, through to the general reader seeking a better understanding of how the world works. She draws on and explains clearly the work of people like Coase, Ostrom and Thaler who have broadened and deepened our understanding of how people both cause and respond to the seven types of failure she describes. The book is furthered enriched, and the lessons consequently rendered more accessible, by a peppering of case studies illustrating the core arguments.

Coyle also tackles government failure, highlighting the shortcomings in bureaucracies (or among public servants) and as a consequence of political failures (or failures of politicians) that result in the application of the wrong policies to address the market failures. The text seems to peter out in the final chapter where she addresses what she appears to hope is the solution to the problems of government failure, which is the application of evidence to economic policy. In this chapter that she reveals the limitations of her experience as a career academic and regulator, with a rather slight addressing of the use of statistics and cost benefit analysis. This doesn’t detract from the power (or readability) of the previous nine chapters, but point to the opportunity for someone else to write something of similar tone and quality to fill the gap on how to test public policy initiatives to address market failure.

The BBC World Service is the insomniac’s salvation. If you are lucky, a background of talk radio helps you back to sleep. If you are luckier still, you stumble on a piece of quality programming that Auntie has chosen to share with the rest of the globe but not with its domestic listeners.

“In the Balance”, a business programme presented by Andy Walker at 03:30 GMT on Sunday 2nd November, included a first class discussion of short termism between Bridget Rosewell, Geoffrey Franklin and Richard Dodds, following an interview with John Kay that marked the second anniversary of the publication of his report for HM Government on short termism in equity markets.¹

The essential conclusion of the Kay report [reference needed] was that there is too much short termism in UK corporate life at the expense of addressing long term competitive advantage. The top management of quoted companies focus unduly on hitting 3 monthly targets, which are a poor measure of management competence, and have been rewarded accordingly. The 1990s featured attempts to align management incentives with the interests of shareholders, but the net result was that “many people who were quite incompetent made quite a lot of money”. Kay concludes that regulation is not the solution, but that a change in culture is required, but that it is hard to know how to do this, and harder still to measure progress.

Kay expanded on the culture change required and the inherent difficulties. He referred to the “marshmallow test”, an experiment with 4 year old children. Most, when presented with a marshmallow and told that if they wait 5 minutes before eating it they will be given a second one, will eat it right away. (A celebrated study of children subjected to the marshmallow found that those who exhibited a lower personal discount rate and exercised sufficient self control to win the second marshmallow – or maybe just had the insight to understand the challenge facing them – prospered more in later life). Andy Walker asked John Kay whether he was saying that executives simply need to grow up, to which Kay responded “a lot of company directors would fail the marshmallow test.”

In the ensuing discussion among the panellists, Bridget Rosewell blamed her profession (economists) for promulgating the view that all the information about the future prospects of the company is captured in the share price, and consequently many board level remuneration packages have been structured around movements in the share price, and the panel as a whole seemed to conclude that we have spent years telling people to focus on the wrong thing. Further, Rosewell also observed that “All markets exist in institutional contexts and cultural contexts.”

Is John Kay right? Undoubtedly yes. But the supplementary questions are more interesting: why do so many fail the marshmallow test; and what can we do about it?

There are probably could be three underlying reasons for the behaviour Kay describes.

One is that, notwithstanding the experimental data that suggests that people who come out on top in later life are those who as small children passed the marshmallow test, perhaps some of those who make it to the upper reaches of commercial organisations respond disproportionately to short term signals. (Or maybe, by the time that they have reached the upper reaches they are no longer capable or responding to anything other than short term signals?). This is not something that I have observed myself, but there may be some revealing academic research lurking in the nether regions of a business school somewhere that addresses the personality types of chief executives and points to this failing.

A second explanation could be that human timeframes and organisational timeframes may be intrinsically misaligned. “In the long run, we are all dead.” The career time horizon for a typical chief is only exceptionally longer than twenty years on first appointment. Even then, the time horizon within the specific appointment is only exceptionally more than ten – and probably for very healthy reasons including personal boredom thresholds and the benefit from time to time for a fresh set of eyes on a problem. Whether it is desirable is irrelevant, it is entirely reasonable for individuals to consider the rewards – both material and emotional – that will flow from what is deliverable and measurable within their own term of office. And although they may also be concerned for their own legacy in the role, they also have to reflect that they have little power to stop those who come after them frittering it away.

The final explanation relates to the institutional and cultural frameworks about which Kay and the “In the Balance” panellists agonised. The evidence here is compelling (although I would not go as far as Rosewell in condemning the argument that share prices capture all the information about a company – the point, for discussion in more depth elsewhere, is that the prices of traded financial instruments are corrupted because they also capture information about expectations about trader behaviour (in an economist’s version of Heisenberg’s Uncertainty Principle). Many management teams have been presented by academics, consultants, brokers, investment bankers, and journalists, arguably in error, that they must respond to and seek to affect short term share price performance, and the regulator environment has encouraged rather than discouraged this. Given that the possibility that the first of these three explanations holds true for some executives, and the probability that the second of these three explanations holds true for most, it is all the more pernicious that the we have aligned cultural and institutional frameworks in this way. Instead, we need to bend over backwards to create a culture and institutional framework as a counterweight to the possibility that personal discount rates – driven by hardwired human appetites and instincts – are higher than those of companies and organisations in general, and society overall.